Nikkei Rebounds on Strong GDP Data

As per the data released overnight, Japan’s GDP expanded more than expected in the final quarter of 2025, with annualized growth of +1.3% in Q4 2025, compared with +1.2% expected and +0.2% in the previous reading. The stronger performance was mainly driven by robust business investment, which increased 1.3% (vs. 0.2% in the flash estimate). Private consumption also improved modestly to 0.3% (vs. 0.1% in the flash estimate). Government spending is expected to rise in the current quarter, while energy subsidies and solid wage growth are likely to support private consumption.

At the same time, household spending unexpectedly fell by 1.0% year-on-year in January (vs. –2.6% in December and +2.4% market consensus). The decline was primarily driven by a sharp drop in housing-related expenditures (–12.3%). However, despite the weak headline figure, underlying spending on goods and private services appears resilient, and wage growth remains solid, with the latest reading showing +1.4% in January. Recent increases in oil prices have been partially absorbed by government measures, with authorities subsidizing oil companies to stabilize gasoline prices: as a result, fuel prices at the pump rose modestly in March (+2.4%). Moreover, as with several other G7 partners, Japanese authorities announced this morning that they are prepared to release strategic oil reserves if necessary.

Overall, the Japanese economy is performing relatively well, supported by declining inflation and rising real wages. Some investors are already beginning to discuss the possibility of another interest rate hike in the coming months, potentially around early summer. Meanwhile, the yen remains very weak (currently around 157.54 against the U.S. dollar), and the Nikkei index is still close to its historical highs, despite the sharp correction seen over the past ten days.

TECHNICAL ANALYSIS

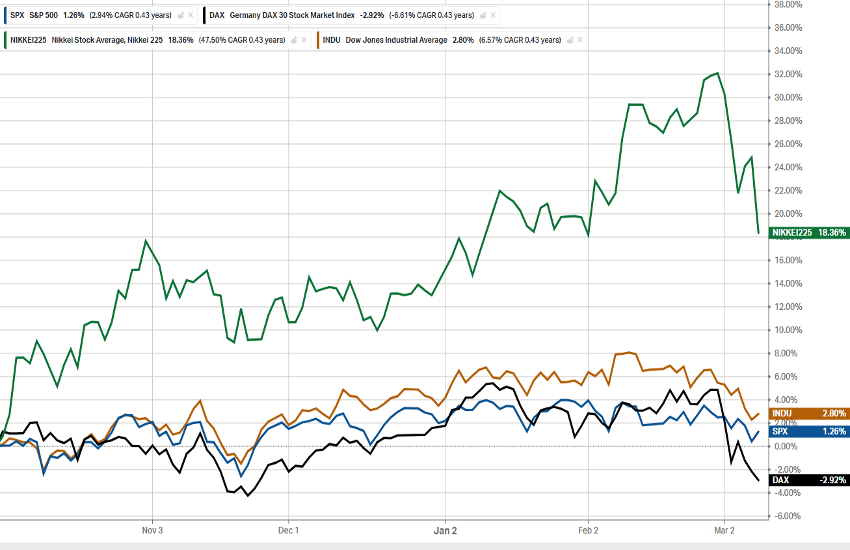

The Nikkei has clearly outperformed its US and European peers in recent months, posting for example a gain of 18.36% since the beginning of October, compared with performances close to flat for the other benchmarks shown in the chart below.

The drop during the turbulence of the past few days has been significant, almost 8,000 points from 59,330 to yesterday’s low at 51,407 (-13.36%), but Trump’s “conciliatory” remarks yesterday (the war could be close to ending, and pressure on Russian oil exports may be temporarily eased) gave fresh momentum to the index, which has risen 6.60% from the low reached at Monday’s opening.

The chart remains fairly orderly and it is somewhat encouraging to note that the bullish cycle that began almost a year ago is still in place. While the trendline was briefly breached yesterday morning, the rebound that followed effectively restored it and the index is now fighting right around that level, trying to hold the 53,850 area. That level and that trendline are decisive for the future direction. Of course this does not depend only on Japanese equities: the weakness of the yen, as mentioned several times, plays its part and the lead of US risk indices has always been a key factor in defining the overall direction. This perhaps worries us slightly, and many commentators suspect that the declines in equity indices have ultimately been rather modest compared with the global economic situation that may be taking shape. In any case, price action is always right, and for now the Nikkei suggests that there is not much to worry about.

The indicators, on the other hand, do not look particularly strong: RSI below 50 and trending downward, the MACD histogram about to turn negative, price below the 21-day moving average and currently struggling around the 50-day moving average. But once again, the key point here is the ability to hold the trendline around 53,900, with immediate strong support slightly lower at 53,500.