Goldman Sachs Kicks Off Earnings Season

Today, before the US market opens, Goldman Sachs will kick off the corporate earnings season.

The financial sector has not performed particularly well this year and is currently the worst-performing sector year-to-date, with the sector ETF XLF down 6.83%. However, the past month has been moderately positive, with gains close to 2%. That said, the prices of major financial names remain relatively elevated and have experienced strong growth throughout 2025 (for example, Goldman Sachs has risen 111% from its last April low to last Friday’s close).

Overall, the sector is trading at P/E levels broadly in line with its 3-year average (12x vs. 12.3x), and earnings are expected to grow by 8.7% annually. This suggests the sector is not particularly cheap, but also not in “bubble” territory. Lower valuation multiples compared to the broader market (the S&P 500 has a long-term P/E closer to 20x) are also within historical norms.

The situation is somewhat different for Goldman Sachs specifically. Its current P/E of 17.9x is about 42% above its 10-year historical average of 12.6x, representing a meaningful premium. The stock is also trading near its 5-year high valuation levels, indicating a premium versus historical norms.

Goldman Sachs is currently trading at a forward P/E of 17x, compared to an industry average of 15.1x. Peers such as JPMorgan trade at around 14x, while Morgan Stanley trades at 15.2x. This confirms that Goldman carries a premium both relative to its own history and its peers.

This premium is largely justified by Goldman’s leadership position in M&A advisory, where it continues to report strong revenue and profit figures. The segment has seen a significant global resurgence in recent years. The firm also leads in equities trading and ranks among the top five global active asset managers. Equity trading revenue reached a record $4.31 billion in Q4 2025, while FICC revenue increased by 12.5%. Goldman’s gross margin of 82.9% is well above industry averages, and its operating margin of 38.3% reflects strong cost discipline at scale.

For today, Wall Street expects a strong quarter:

- Revenue consensus: $17.01 billion, implying +12.9% year-over-year growth

- EPS consensus: $16.14–$16.86, representing roughly +14–17% growth vs. Q1 2025.Goldman has beaten EPS estimates in each of the past four quarters, with an average earnings surprise of 14%

- Investment Banking fees: $2.6 billion, expected to be up 33% YoY, driven by a rebound in M&A and IPO activity

- Net Interest Income: around $3.7 billion, up 27% YoY

- Options market pricing: implies a ~5.8% move in either direction following earnings

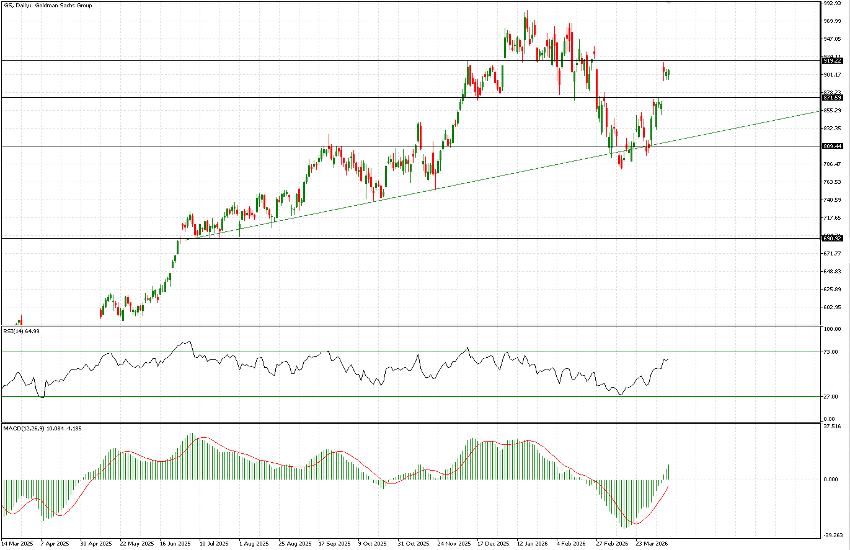

TECHNICAL ANALYSIS

Focusing on the past few months, we observe a fairly moderate medium-term uptrend. Valuations were around $700 in May 2025 and reached $800 a couple of weeks ago, over a span of roughly 10 months.

The chart does not differ significantly from that of the S&P 500, showing a consolidation phase near the highs between November and early February (shorter than the index’s), followed by a late-winter pullback. We are now back testing what had been one of the key support levels that previously held prices elevated during the consolidation phase (possibly a distribution phase).

Between March 11 and March 31, this trendline we identified was tested multiple times and briefly broken, but ultimately held, allowing prices to rebound.

As of Friday’s close at $905.92, the price is positioned between two key levels: $919 and $871. Notably, the implied move from options markets suggests that the opening price could break beyond these levels, effectively clearing them.

On the downside, the next levels to watch are $845–$850, followed by $830, and then around $815, which is where our trendline currently sits. On the upside, we are also monitoring approximately $935 and $960, not far from the all-time high of $983.

Technical indicators -RSI and MACD- are currently positive.