Oil Supply Shock Signals Longer-Term Disruption

Yesterday, oil prices declined, with the Brent benchmark falling by 2.84% to $100.21 and WTI dropping by 5.27% to $93.50. Among other factors, this confirms our view from a few days ago—a renewed widening of the WTI–Brent spread toward $7 after reaching parity last Monday. However, the focus now shifts to broader supply dynamics.

The global market entered this crisis with an oversupply of oil: approximately 106 million barrels per day were being produced, while demand stood at around 102.5–103 million. This imbalance justified relatively subdued price levels over a longer-term horizon. However, after accounting for flows redirected via pipelines to bypass the Strait of Hormuz, up to 15 million barrels per day of supply are currently disrupted, creating a significant daily deficit. These volumes are unlikely to return to the market in the short term.

Ongoing conflict continues to constrain production, while onshore storage facilities are reaching capacity. The United States has proposed both insurance coverage for tankers transiting the strait—currently unavailable in the market—and naval escorts, although neither measure has yet been implemented. Even under optimistic assumptions, escort operations are unlikely to begin before the end of March, given the intensity of the situation.

Global supply elasticity remains limited. Key producers such as Saudi Arabia and Russia are currently unable to increase output, despite the temporary easing of U.S. sanctions on Russian oil aimed at allowing floating cargoes to reach buyers and support some Asian refiners. U.S. production is expected to remain broadly flat in 2026, with only around 500,000 additional barrels per day potentially coming online in 2027.

Offsetting these constraints—and contributing to yesterday’s price decline—more than 30 countries have agreed to release a total of 400 million barrels from strategic reserves. The United States alone will contribute 172 million barrels from its Strategic Petroleum Reserve. However, this remains a temporary measure: with a deficit of 15 million barrels per day, these reserves would cover roughly 25 days of supply.

Two additional developments also contributed to the recent decline. The Aframax tanker Karachi, carrying Abu Dhabi’s Das crude, became the first non-Iranian cargo tanker observed transiting the Strait of Hormuz while broadcasting its AIS signal since the crisis began, marking a tentative step toward normalization. Notably, the cargo was reportedly settled in yuan rather than U.S. dollars. In addition, U.S. Treasury Secretary Scott Bessent indicated that Iranian oil tankers are being allowed to transit the strait, stating that “the Iranian ships have been getting out already, and we’ve let that happen to supply the rest of the world.”

In summary, while several factors contributed to the recent price pullback, these appear to be temporary. The base case remains that elevated tensions will persist for several weeks, potentially followed by a lower-intensity phase involving diplomatic engagement. Only at that stage might producers begin to consider increasing output, a process that is operationally complex and cannot be implemented immediately. As such, normalization may not occur until well into Q2, even under optimistic assumptions. A more prolonged disruption would likely require a significant contraction in global demand, implying a broader economic slowdown.

TECHNICAL ANALYSIS

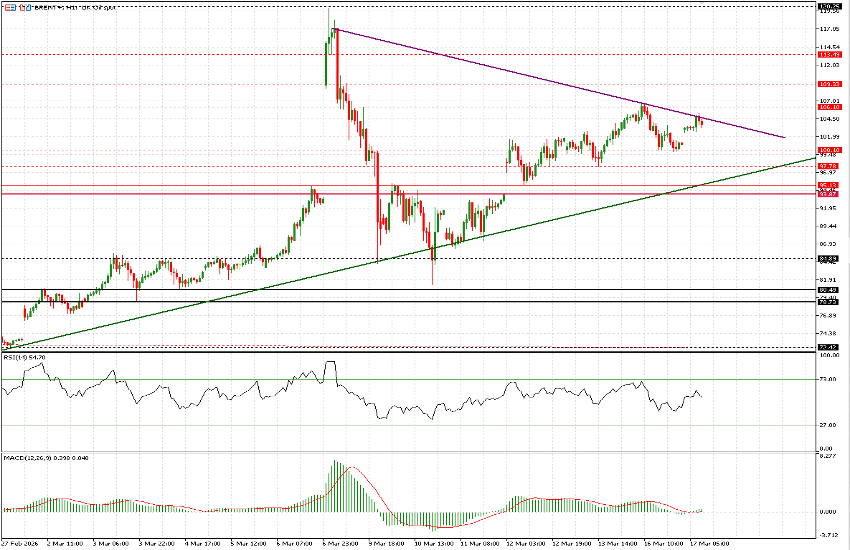

Brent is trading higher this morning, up 2.23%. While the 1-hour chart is used to identify short-term entry points and risk parameters, it is important to note that on the daily timeframe the RSI remains deeply overbought at 88. Today’s candle is attempting to return within the Bollinger Bands, following several sessions trading outside them since the initial escalation (with the exception of March 10–11).

On the 1-hour chart, the trendline originating on February 27 continues to act as a key support reference. Even in the event of a pullback, this level is expected to represent the final barrier before a potential continuation higher. In recent sessions, price has consolidated within a range between $97.80 and approximately $106.

At present, a downward-sloping trendline near $104.70 is in focus. A break above this level would increase the probability of a move through $106–$106.50, with initial upside targets at $109.30, followed by $113.50, and finally the previous highs at $120.

However, there could be several days of consolidation, coinciding with the ongoing release of reserves and hopes for agreements on traffic through Hormuz. On the downside, we are closely watching $102.50, $100.10, and $97.80. We consider it unlikely that the price will fall below $95.15 / $94. These levels may seem far apart, but volatility is significant. We always recommend avoiding trading the news and maintaining clearly defined levels.